Fitch does not see EFSF plans changing France's AAA Rating

European stocks were slightly up in the early session before Fitch announced that it does not see changes to the European Financial Stability Facility as a threat to France's AAA rating, and that a strong EU solution would likely preserve Spain's and Italy's ratings as well. Following Fitch's announcement the DAX Index jumped 1.7 percent.

GE meets expectations on finance unit; McDonald's delivers as always

GE reports 3Q operating EPS 0.31 in line with estimates of 0.31 as improvements in GE Capital offset weakness and margin contraction in its energy division. Investors are slightly disappointed sending the shares down 1.4 percent in pre-market trading.

McDonald's delivers what the market always wants, namely better-than-expected earnings, as the company reports 3Q EPS 1.45 beating estimates of 1.43 driven by market-share gains across the globe. The shares are up 2.9 percent in pre-market trading.

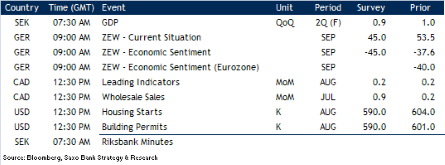

Other earnings releases out in pre-market are:

European stocks were slightly up in the early session before Fitch announced that it does not see changes to the European Financial Stability Facility as a threat to France's AAA rating, and that a strong EU solution would likely preserve Spain's and Italy's ratings as well. Following Fitch's announcement the DAX Index jumped 1.7 percent.

GE meets expectations on finance unit; McDonald's delivers as always

GE reports 3Q operating EPS 0.31 in line with estimates of 0.31 as improvements in GE Capital offset weakness and margin contraction in its energy division. Investors are slightly disappointed sending the shares down 1.4 percent in pre-market trading.

McDonald's delivers what the market always wants, namely better-than-expected earnings, as the company reports 3Q EPS 1.45 beating estimates of 1.43 driven by market-share gains across the globe. The shares are up 2.9 percent in pre-market trading.

Other earnings releases out in pre-market are:

- Schlumberger reports 3Q operating EPS from continued operations of 0.98 missing estimates of 1.01.

- Verizon reports 3Q operating EPS 0.56 beating estimates 0.55