What a dramatic week for the Swiss franc. Much has been written over

the last few days on the Swiss National Bank's actions, pushing EURCHF

spot from the 1.1200 all the way to where we are now (1.2150), firmly

above the 1.2000 floor. In our previous article, we highlighted the

implied volatility price action during the CHF strengthening, and the

all important interests to purchase EURCHF upside options seen prior to

the move up in spot.

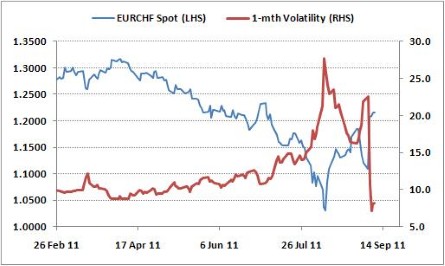

So what happened to EURCHF implied volatilities recently? Well,

movements have been as dramatic as they have been in the spot market.

The below chart shows 1mth EURCHF implied volatility together with the

spot price.

EUR/CHF - Spot and 1mth implied Volatility

(source Bloomberg)

Several points should be made:

- EURCHF implied volatilities reached record high with spot dropping to the lows.

- Volatilities collapsed after the SNB action. It should therefore be noted that, so far, the Central Bank’s actions have proven very successful. As per usual, central banks are not only complaining about currencies being under or overvalued, they also strongly argue against excessive volatility in financial markets. To that extent, SNB has hit home run!

- As seen on the above chart, 1-month volatility fell from around 22% before the SNB intervention to about 8.5% at time of writing. Similar moves have been observed across the curve, with 1-year, for instance, dropping from 17% to 10.5%

- We are seeing continued interest to sell EUR puts with strikes below 1.2000, from both end-users and interbank players. Indeed, with a supposed floor at this level, selling such options and collecting the premium is seen as a risk-free trade. A word of warning though… there is no such thing as a risk-free trade, and such strategies could prove very costly if the SNB is unable to defend this level, or, for instance, if it decides to adjust the floor level.

- Over the last couple of days, we saw an interesting development in the option market: implied volatilities are gaining ground when spot drifts higher - rather than lower. So far those moves in implied volatilities have been muted, but this is a large shift in sentiment from the FX options market.

- As a result, risk-reversals have changed dramatically as well: 1month risk-reversal is now favoring the upside (0.80% middle)… those were quoted around 3.5 vols favoring downside prior to the move in spot!

- Liquidity in the EURCHF FX options market has been extremely poor over the week, and is only slowly returning to normal.

No comments:

Post a Comment